The 8-K Test: Public DST Sponsor Due Diligence

A four-business-day SEC disclosure rule turns sponsor monitoring from quarterly storytelling into structured early warning. Here’s how to use it.

When an advisor recommends a DST replacement to a 1031 client, the sponsor due diligence question that should keep you up at night isn’t “how good are this sponsor’s offerings today?” It’s “how will I know when something has gone wrong?”

That single question separates public-company DST sponsors from private ones in a way most due diligence frameworks miss. And the answer, mechanically, is Form 8-K.

What an 8-K Is, in 90 Seconds

A Form 8-K is the SEC’s “current report” filing. Public reporting companies must submit it within four business days of certain material events. Unlike the 10-K (annual) and 10-Q (quarterly), which are scheduled, the 8-K is event-driven. Something happened. The company has 96 hours to tell you about it.

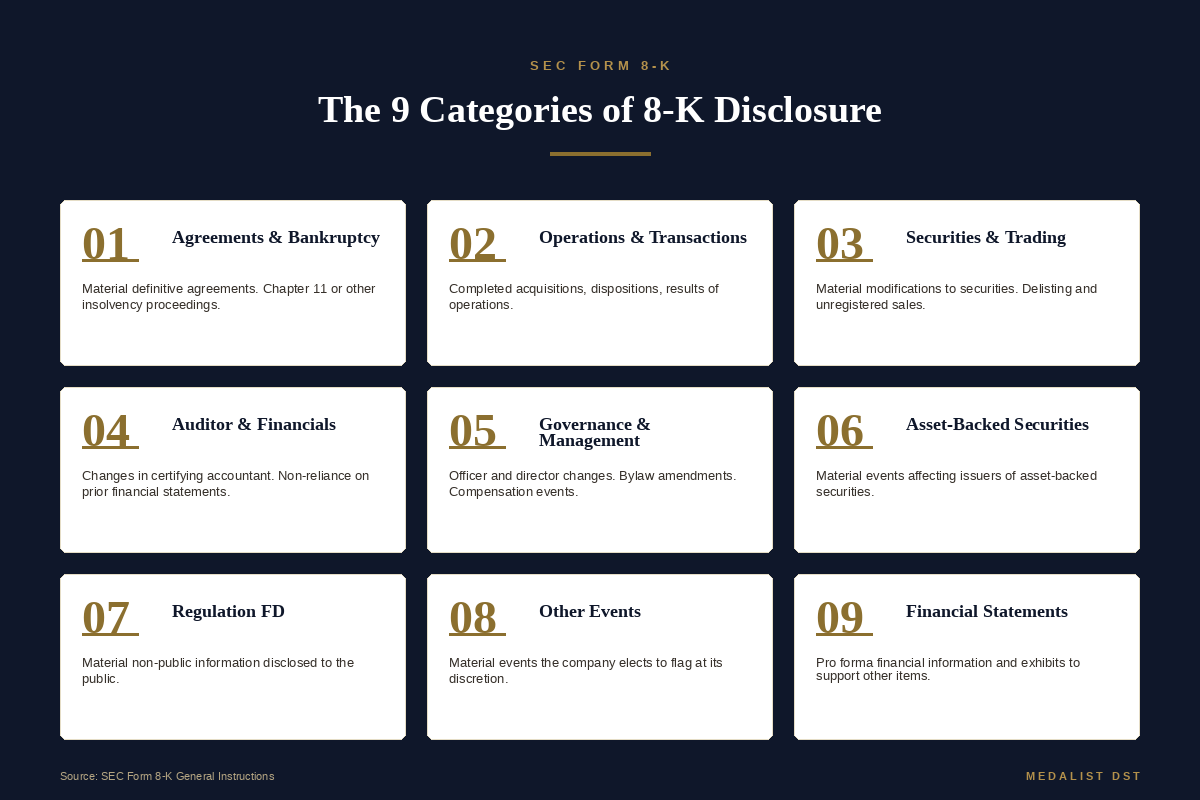

The events that trigger an 8-K aren’t trivia. The SEC has defined a specific list of disclosure items, organized into nine categories:

Item 1 series: material definitive agreements, bankruptcy

Item 2 series: completion of acquisitions or dispositions, results of operations

Item 3 series: securities and trading

Item 4 series: changes in registrant’s certifying accountant, non-reliance on previously issued financial statements

Item 5 series: corporate governance and management changes

Item 6 series: asset-backed securities events

Item 7 series: Regulation FD disclosures

Item 8 series: other events the company elects to flag

Item 9 series: financial statements and exhibits

For a DST sponsor that’s a public reporting company, this list functions as an early-warning system. Material related-party transactions. Executive departures. Loan covenant violations. Auditor disagreements. Property impairments. They all hit 8-K, on the public record, within four business days.

The Asymmetry With Private Sponsors

Private DST sponsors aren’t required to file anything publicly. The PPM is current as of the date it was written. After the offering closes, your visibility into the sponsor’s operations narrows to whatever the sponsor chooses to tell you in quarterly reports, on whatever cadence the sponsor selects.

If the sponsor’s CEO leaves, if a key lender walks away, if a related party is sued, if an auditor resigns, none of these events have to reach you on any defined timeline.

This isn’t a theoretical risk. Several well-known DST sponsor failures over the past decade share the same pattern: the operational problems were known internally for months before investors learned about them. The information existed. It just wasn’t required to surface.

The 8-K requirement collapses that gap. For a NASDAQ-listed sponsor, the information surfaces within four business days. Full stop.

Four 8-K Items Worth Setting Alerts For

If you’re serving 1031 clients with DST exposure to any public-company sponsor, four specific 8-K items deserve standing attention.

Item 1.03, Bankruptcy or Receivership. The most obvious. Any commencement of proceedings under Chapter 11, Chapter 7, or analogous insolvency law triggers this. You’ll know inside a week.

Item 4.01, Changes in Registrant’s Certifying Accountant. Auditor changes are one of the loudest accounting red flags in any industry. An auditor that resigns or is dismissed mid-cycle requires immediate disclosure, plus an explanation of any disagreements with management. Reading these explanations carefully has saved careful investors from disasters more than once.

Item 5.02, Departure of Directors or Certain Officers. Executive and board turnover at a small public DST sponsor is information worth having quickly, but the value is in the context the filing provides, not the headline. An unexplained mid-cycle departure of a CEO, CFO, or chief investment officer reads very differently from a governance change a company discloses as part of a stated strategic transition. The filing itself usually tells you which one you are looking at. The discipline is to read that context before reacting to it.

Item 7.01, Regulation FD Disclosure. This is the category for material non-public information the company chooses to disclose publicly. Distribution announcements, property updates, financing closings, and similar items often appear here.

How to monitor them, free: SEC EDGAR has an RSS subscription system that pushes 8-K filings for any registrant directly into your reader or inbox. Subscribe once per public DST sponsor where you have client exposure, and you’ll know about every event the moment it’s filed.

For the broader 1031 sponsor diligence framework, see Sponsor Due Diligence Questions on my1031options.com.

How to Read an 8-K in Five Minutes

The 8-K format makes this fast. Every filing follows the same structure:

Cover page identifies the registrant

Item heading tells you what category of event triggered the filing

Item body describes the specific event in plain English

Exhibits include the underlying documents (loan agreements, press releases, severance agreements)

A typical 8-K is two to four pages of text. The item heading alone tells you in 30 seconds whether the filing matters for your client. If it’s an Item 8.01 announcing a charitable contribution, you can move on. If it’s an Item 4.01 announcing an auditor change, you have homework.

The discipline that matters: read the actual filing rather than relying on a press release. Press releases describe events through the sponsor’s preferred lens. The 8-K language is governed by SEC disclosure requirements and tends to be more clinical and complete. The two together give you the full picture.

Reading a Sponsor in Transition

One scenario deserves its own note, because it is where mechanical screening misfires most often. A sponsor that is deliberately repositioning its business will generate a cluster of filings in a short window: asset dispositions, debt retirement, governance adjustments, and a restatement of strategy. Read item by item, out of context, that activity can look like instability. Read together, against a transition the company has disclosed and explained, it is the opposite. It is the company executing a plan in full public view, with each step documented on the record as it happens.

The signal you are actually screening for is not activity. It is activity with no disclosed rationale, or a pattern of changes the company declines to explain. A sponsor mid-transition that files early, files completely, and states plainly that its governance and portfolio moves are part of a board-approved strategy is giving you more information than a static private offering ever will, not less. The mechanical screen flags the volume of filings. The careful reader checks whether the volume has a stated reason. That difference is the entire point of having the filings at all.

What This Means for Advisor Client Conversations

When a 1031 client asks why you’re recommending a particular DST replacement, the answer typically includes property quality, sponsor track record, fee structure, and projected hold. Adding “and I can monitor material events on this sponsor through public filings on a four-business-day disclosure cycle” is a fundamentally different sentence than what advisors using only private sponsors can say.

It also gives the client an enduring deliverable. They can subscribe to the sponsor’s EDGAR feed themselves. They become a participant in monitoring their investment, not a passive recipient of quarterly statements written months after the fact.

This is part of why many sophisticated 1031 advisor practices prefer public-company DST sponsors when available, not because public companies are inherently better operated, but because the information environment is structurally different. You see what you need to see, when you need to see it.

The Practical Recommendation

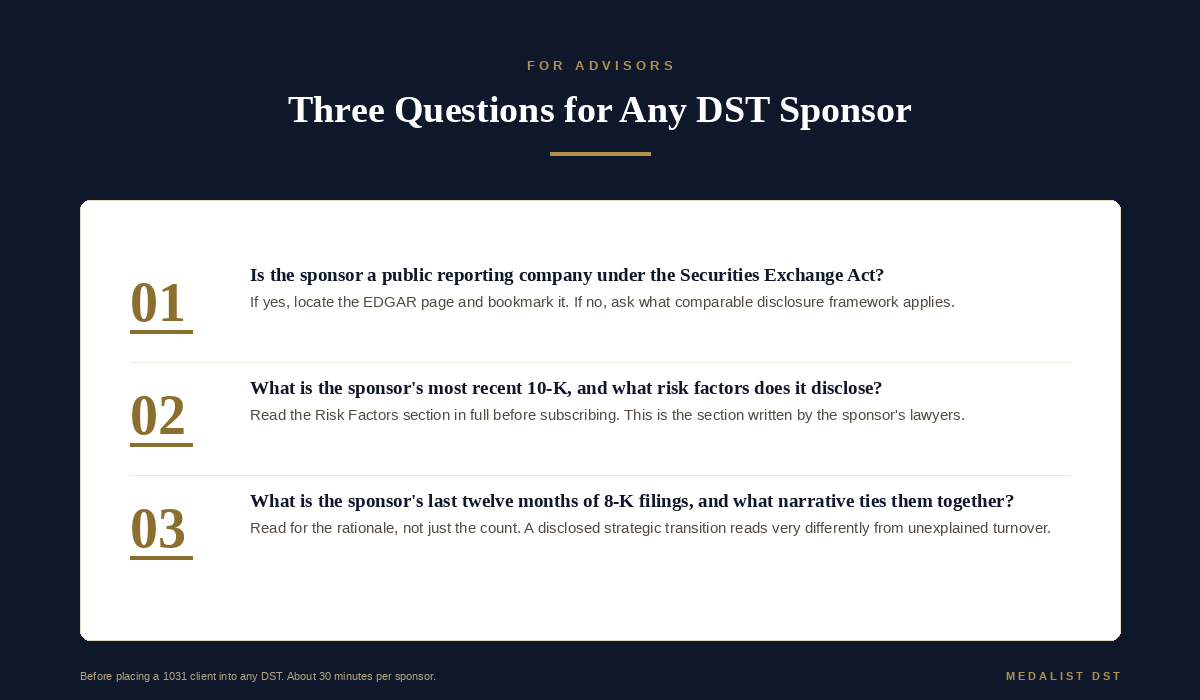

Before placing any 1031 client into a DST, ask three questions about the sponsor’s information environment.

Is the sponsor a public reporting company under the Securities Exchange Act? If yes, locate the EDGAR page and bookmark it. If no, ask what comparable disclosure framework applies and on what cadence.

What is the sponsor’s most recent 10-K, and what risk factors does it disclose? Read the Risk Factors section in full before subscribing. This is the one section of the 10-K written specifically by the sponsor’s lawyers to surface what they thought was significant enough to disclose in writing.

What is the sponsor’s last twelve months of 8-K filings, and is there a stated narrative that ties them together? Repeated officer or auditor changes that the company does not explain are worth examining before placing additional client capital. The same filings, when they trace a disclosed strategic transition, tell you the opposite: that you are watching a documented plan unfold rather than discovering surprises after the fact. Read for the rationale, not just the count.

These three checks take about thirty minutes per sponsor and would catch most of the deteriorating-sponsor scenarios that have hurt 1031 clients in the past decade.

For 1031 clients who need the foundation first, what a DST is, how the 1031 timeline works, and why sponsor selection matters at all, the Sponsor Evaluation Framework and Sponsor Due Diligence Questions on my1031options.com are structured to be sharable directly with the client as pre-call homework.

The four-business-day cycle is the simplest, most underused due diligence tool in the DST advisor’s stack. It’s free, it’s public, and it’s exactly what it was designed to be.

Medalist Diversified, Inc. (NASDAQ: MDRR) is a public reporting company subject to the SEC’s 8-K filing requirements. Medalist is in the midst of a disclosed, board-approved repositioning from a diversified REIT into a Delaware Statutory Trust sponsor platform, and every step of that transition, including portfolio dispositions and governance changes, is documented on the public record. We invite advisors and their clients to verify our filings on EDGAR and to read them for what they are: a strategy executed in full public view, on a four-business-day disclosure cycle. This article is educational and not a recommendation of any specific security. Securities are offered only by means of a Private Placement Memorandum to accredited investors as defined in Rule 501 of Regulation D.